{kind=link}

Decarbonisation. Net zero. Carbon neutral. These terms are synonymous with achievement of the goals outlined in the Paris agreement. If we are to avoid catastrophic changes to our climate then they are also terms which must become standard, and non-negotiable.

KPMG Climate Change & Carbon Manager David Sandrussi.

Decarbonisation targets, including net zero and beyond, are being pursued at an increasing rate by governments, within industrial sectors and by individual businesses. The retail sector is no exception. Customers increasingly demand that carbon footprint is as important to the retailers they shop with as bottom line, investors insist on transparency around ESG metrics, and partners want to be part of a low carbon value chain.

Guiding retail leaders in the creation of decarbonisation targets is an exercise in business case development. They demand that economic growth and carbon emissions are decoupled; they must be, if we are to have any chance of meeting global economic development goals, as well as those set out in the Paris agreement. Fortunately, it is increasingly evident that decarbonisation and sustainability are contributing to increased market share and revenues. Being purpose-driven is a competitive advantage. For example, Unilever’s Sustainable Living brands outperform the average growth rate of the rest of their portfolio, and are reported to have avoided over €1 billion in costs by using less material and producing less waste.

For retailers looking to decarbonise there are five key steps to consider:

- Making greenhouse gas metrics visible

The backbone of retail decarbonisation lies in emissions visibility. Establishing a baseline and measuring ongoing emissions is vital. Challenges exist, particularly in addressing the complexity of scope 3 emissions – those produced indirectly within a value chain, such as by business partners. However, they are surmountable. For example, it is possible to use spend-based data (eg, dollars spent on delivery of raw materials) to calculate scope 3 emissions if data is not available from partners.

- Minimising logistics-related emissions

Supply chain emissions are often the largest contributor to a retailer’s carbon footprint. I worked with an e-commerce retailer who sold products made in Asia to customers throughout Europe; 92% of their emissions were logistics related. By selecting inputs into the final goods, they sell or sourcing final goods closer to the manufacturing location and/or their customers, emissions can be significantly reduced.

- Doing more with less

Resource use can make or break a retailer’s decarbonisation strategy, and their bottom line. Efficiency can result in positive triple bottom line outcomes; fewer emissions, resource preservation and economic benefits. But ‘doing more with less’ has its challenges. Enhancing product quality while maintaining prices and reducing inputs requires creativity. Finding ways to reuse and recycle product inputs, or product input substitution (think Australian-grown coffee beans instead of those sourced in Colombia) are key. Done well, this can result in first mover advantage and the associated benefits, including the right to charge premium prices and customer loyalty.

- Embracing renewable energy

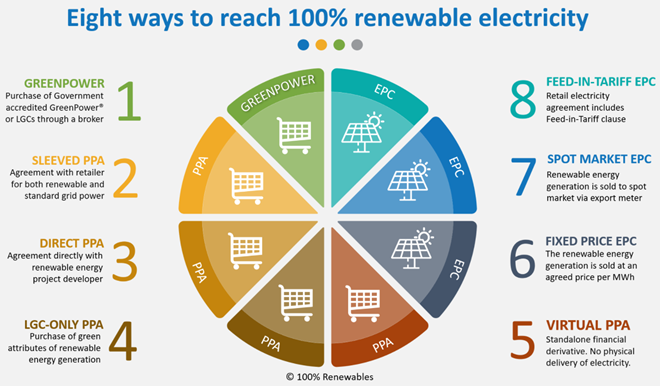

Retailers may find their scope 2 emissions (produced by purchased energy) to be a large contributor to their carbon footprint. While the domestic price gap between fossil fuel and renewable energy is shrinking, some still feel accessing 100% renewable energy is cost prohibitive. The good news is that there are affordable solutions for those aiming to achieve net zero energy emissions:

While the cost of purchasing 100% GreenPower remains around 5-8 cents per KWh more than the current average electricity rate, these prices can be reduced through combining GreenPower and feed-in-tariffs available to retailers who invest in renewable energy infrastructure via onsite purchase power agreements (PPA’s).

- Reducing waste

Growing sales while reducing waste is key. Retailers are increasingly considering this problem when designing products and services by adopting circular economy principles. Eliminating waste in the design phase can have triple bottom line impact, while providing a point of differentiation; creating a unique take on familiar products and uncovering additional revenues. Renault have created Europe’s first circular economy factory for vehicles; remanufacturing components, increasing recycled plastic content and creating a second life for electric batteries. These activities generated revenues of nearly €120 million in 2019, while producing 70% less waste.

Decarbonisation provides unique challenges for retailers. However, these five steps provide a strong starting point for any business trying to reduce their carbon footprint and benefit from a low carbon operating model.

About David Sandrussi

David Sandrussi is a manager within KPMG’s Sustainability and Climate Change team in Melbourne. He specialises in corporate decarbonisation strategy, with a particular focus on sustainable innovation that supports the synthesised achievement of emission reduction and commercial growth. Having previously led the decarbonisation strategy for one of Europe’s largest e-commerce retailers, his experience includes net zero strategy, carbon and climate risk management strategy, carbon accounting (including scope 3), and low-carbon product development.